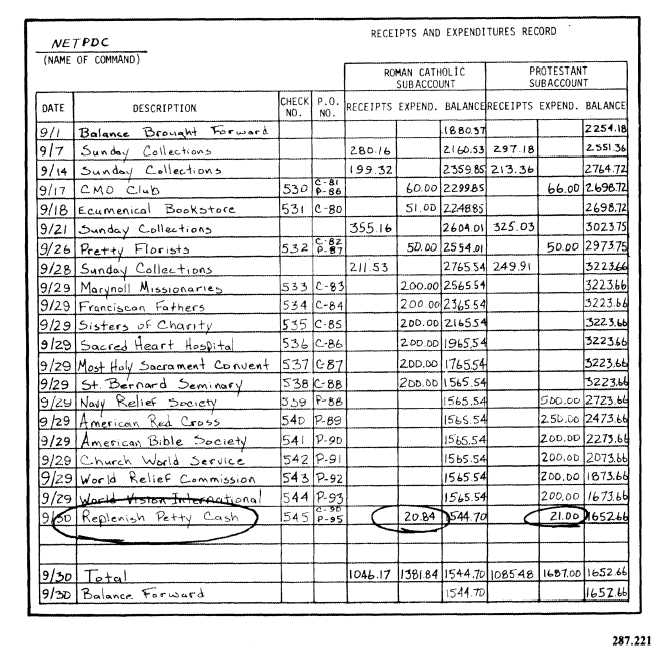

entry, such as the one shown in figure 4-27, is

made on the Receipts and Expenditures Record

to show that a petty cash fund has been

established. The disbursements from each sub-

account that established the petty cash fund

are posted by memorandum entry only in each

individual account, since the composite balance,

or the net worth of the religious offerings fund,

is not affected.

The central petty cash fund should be

often if necessary. Faith group subaccount custo-

dians who have authorized the disbursement of

funds from the central petty cash fund should en-

sure that a purchase order for the amount used is

prepared by the religious offerings fund ac-

countant. This document is then submitted to the

religious offerings fund administrator, who should

ensure that a check is drawn against that sub-

account in the appropriate amount to replenish the

central petty cash fund up to the original amount

replenished at the end of each month or more

of . Figure 4-28 illustrates this process.

Figure 4-28.—Record of Receipts and Expenditures entry replenishing petty cash.

4-27