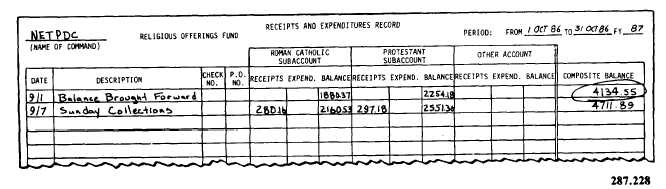

figure 4-35.—Receipts and Expenditures Record entry showing composite balance carried over to the next month.

Obligations or commitments in excess of

current CASH assets of the fund

AUDITS OF THE RELIGIOUS

OFFERINGS FUND

An audit of the religious offerings fund may

be ordered by the ccommanding officer at anytime.

An auditor will be appointed by the commanding

officer for this purpose.

The auditor submits the formal audit findings

in writing to the commanding officer and the

command chaplain after the audit is completed.

A copy should be retained as part of the

financial records of the religious offerings fund.

Religious offerings funds at Marine Corps

installations will be audited at the end of each

quarter by the area auditor. Formal audit findings

from these area auditors are submitted in a

manner similar to that used by Navy units. Audits

may be ordered at the following times:

At the close of the fiscal year

When the religious offerings fund admin-

istrator is relieved

When a religious offerings fund sub-

acount custodian is relived (partial audit)

When the religious offerings fund is

dissolved

PREPARING FOR AN AUDIT

Auditing procedures may vary slightly from

command to command. However, the RPC or

RP1 should determine the following from time

to time and before an audit:

Do bank deposit slips, checkbook, and

bank statement balances all agree?

Does the sum of all account balances on

the Receipts and Expenditures Record equal the

composite balance?

Does the opening composite balance, plus

all receipts, minus all expenditures, equal the

closing composite balance as recorded on the

Receipts and Expenditures Record?

Have all purchases drawn from the reli-

gious offerings fund been substantiated by

consecutively numbered purchase orders that have

been signed by the fund administrator?

Has the commanding officer authorized

the establishment of a petty cash fund to make

miscellaneous purchases?

Has the petty cash fund been replenished

monthly, or made often if necessary, by each

subaccount as disbursements have been made?

Has the religious offerings fund admin-

istration been appointed in writing by the com-

manding officer?

Have the various faith groups in the

Command Religious Program been authorized in

writing by the commanding officer to maintain

separate subaccounts within the religious offer-

ings fund?

4-35