Data Blocks L - V

(REMARKS)

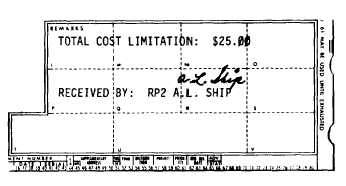

A total cost limitation and the signature of

the person receiving the material must be entered

in the “REMARKS” section for SERVMART

requisitions. RP2 A. L. Ship prepared this

requisition and estimated that the total cost of

the supplies would be approximately .

Figure II-2-16 shows some of the important

“Do’s

of

MILSTRIP

requisitioning.”

Regardless of whether an ecclesiastical item is

being ordered or a SERVMART “run” is being

made, the RP should ensure that the DD Form

1348 is properly filled out. Remember, the

storekeeper in the supply department will pro-

vide assistance upon request. It is imperative

that the RP utilize this source of information

when ecclesiastical items are being procured.

INVENTORY FUNCTIONS

The term “inventory” is defined as either the

quantity of stock on hand for which stock

records are maintained; or, the function

whereby material on hand is physically inspected

and counted, and stock records are reconciled

accordingly. The RP plays a vital part in

accounting for supplies and material once they

have been procured. However, advisory

assistance for inventorying the material in the

custody of the office of the chaplain should

always be, obtained from the personnel in the

supply department.

The next few sections will be devoted to

defining certain

inventory terms; and, to

explaining some of the requirements and pro-

cedures for conducting an inventory of supplies

and material.

EQUIPAGE

Equipage is a term applied to items that are

not consumed in use, and are usually of greater

value and have a longer life than supplies. There

are two types of equipage: controlled equipage

and other equipage.

Controlled Equipage

Controlled equipage consists of items which

require increased management control due to

high cost, vulnerability to pilferage, or impor-

tance to the command’s mission. Tape

recorders,

c a l c u l a t i n g m a c h i n e s , a nd

typewriters, either manual or electric, are a few

examples of controlled equipage. The personnel

in the supply department maintain a master list,

by department, of all controlled equipage for

each command. The RP should keep accurate

records to ensure that the controlled equipage

maintained in the office of the chaplain matches

the master list maintained in the supply depart-

ment. This can be accomplished through the

maintenance of an index card file system or by

other similar methods. Figure II-2-17 illustrates

an example of the index card method of

accounting for controlled equipage. The RP

should check all the items of controlled equipage

in the index card file for the Command Religious

Program with the master list maintained in the

supply department to ensure that these two lists

reflect the same information.

Other Equipage

Other equipage consists of items which are

not controlled and are procured in the same

manner as other operating space items (con-

sumable supplies). Requests for other equipage

items are submitted directly to the supply activ-

ity as in the case of the “Candlelighter and Snuf-

fer” which was ordered from the Defense

General Supply Center, Richmond, Virginia.

2-27